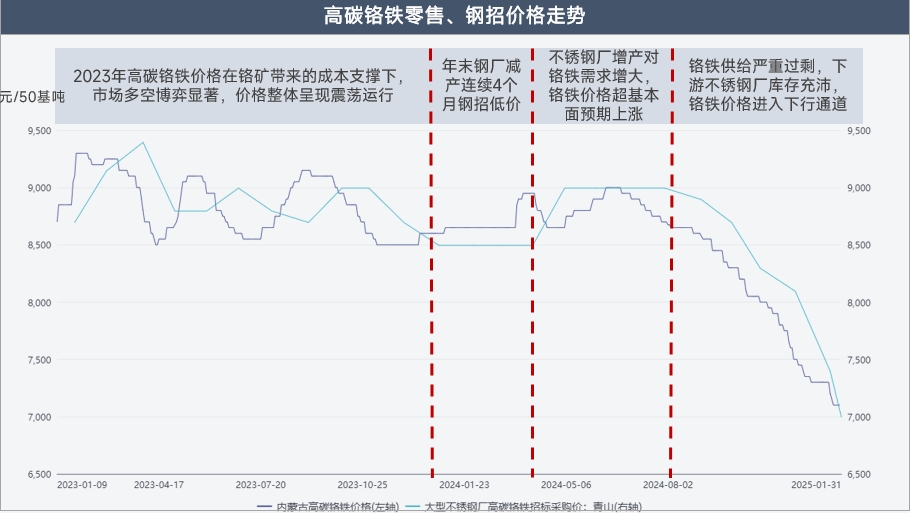

Review of High-Carbon Ferrochrome Price Trends

With the end of pandemic controls in 2023, the domestic economy oscillated between strong expectations and weak realities. High-carbon ferrochrome prices experienced narrow fluctuations throughout the year, supported by costs and robust supply and demand, remaining at a relatively high level overall.

From December 2023 to March 2024, the bidding prices of mainstream stainless steel mills remained flat at low levels for four consecutive months, leaving the ferrochrome market stagnant, with retail prices also staying flat for an extended period.

In April 2024, Tsingshan announced its steel bidding prices in mid-March, exceeding market expectations with a sharp increase of 500 yuan/mt (50% metal content). The prices then remained stable for the following four months, revitalizing activity in the ferrochrome market.

Starting in August 2024, bidding prices entered a downward trajectory, with a cumulative decline of 2,000 yuan/mt (50% metal content) from August 2024 to January 2025.

Analysis of China's High-Carbon Ferrochrome Supply

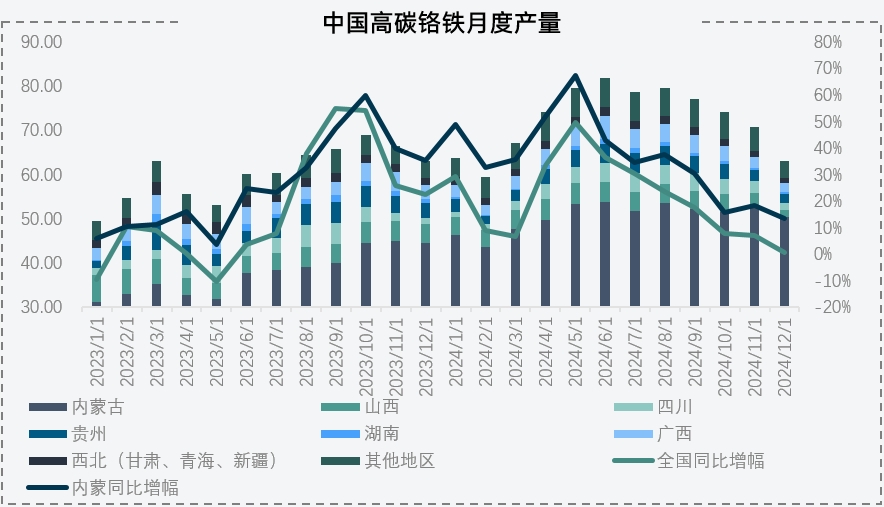

High-carbon ferrochrome production in 2024 saw a significant increase, reaching a historical high of over 800,000 mt in June. Annual production reached 8.56 million mt, up 1.4442 million mt YoY, an increase of 19.94%. In Inner Mongolia, production exceeded 6 million mt, up 1.53 million mt YoY, an increase of 34%.

This year, ferrochrome production showed notable growth, primarily concentrated in Inner Mongolia. As the main production base for ferrochrome, Inner Mongolia's position is indisputable. Benefiting from locational advantages, its average monthly production exceeded 500,000 mt, accounting for about 70% of the national total.

Several unique advantages make Inner Mongolia difficult to surpass. First, electricity costs in Inner Mongolia are relatively low, currently at 0.39-0.42 yuan per kWh, compared to over 0.6 yuan in southern regions. Second, its proximity to Tianjin Port results in lower logistics costs, with average freight from Tianjin Port to Ulanqab at about 80 yuan/mt, compared to over 200 yuan in southern regions. Additionally, as a major coke production base, Inner Mongolia enjoys significant price advantages, while southern regions often need to procure and transport coke from Shaanxi, Shanxi, or even Xinjiang. Lastly, strong support from local governments is another advantage, with Ulanqab City designating the ferroalloy industry as a key pillar for development. Driven by these advantages, Inner Mongolia's share of ferrochrome production is expected to continue expanding in the future.

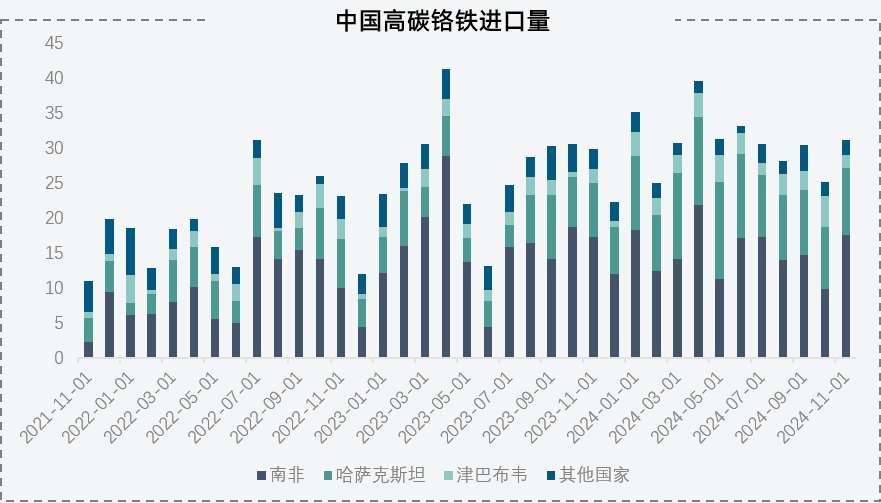

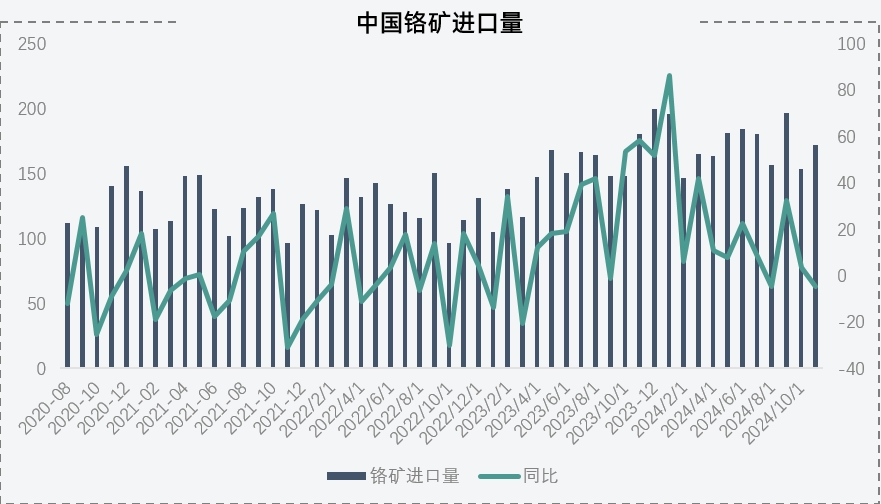

From January to November 2024, cumulative imports of high-carbon ferrochrome reached 3.398 million mt, up 370,000 mt YoY, an increase of 12.54%. South Africa remained the primary supplier with stable import volumes, while growth mainly came from Kazakhstan and Zimbabwe.

Overseas demand for high-carbon ferrochrome has declined. Tsingshan Group's high-carbon ferrochrome project in Indonesia, with an annual capacity of 1.2 million mt, commenced production from late 2023 to 2024, partially replacing the need for ferrochrome imports for local stainless steel production lines.

Kazakhstan has become the main contributor to China's ferrochrome import growth, thanks to the recovery of logistics after the pandemic and the gradual normalization of transportation through the Alashankou Pass. Additionally, declining stainless steel production in European countries has redirected significant volumes of Kazakhstan's high-carbon ferrochrome to China. Meanwhile, Zimbabwe's ferrochrome production has increased due to substantial Chinese investments. Ferrochrome imports are expected to remain at high levels and stabilize in the future.

Analysis of China's High-Carbon Ferrochrome Demand

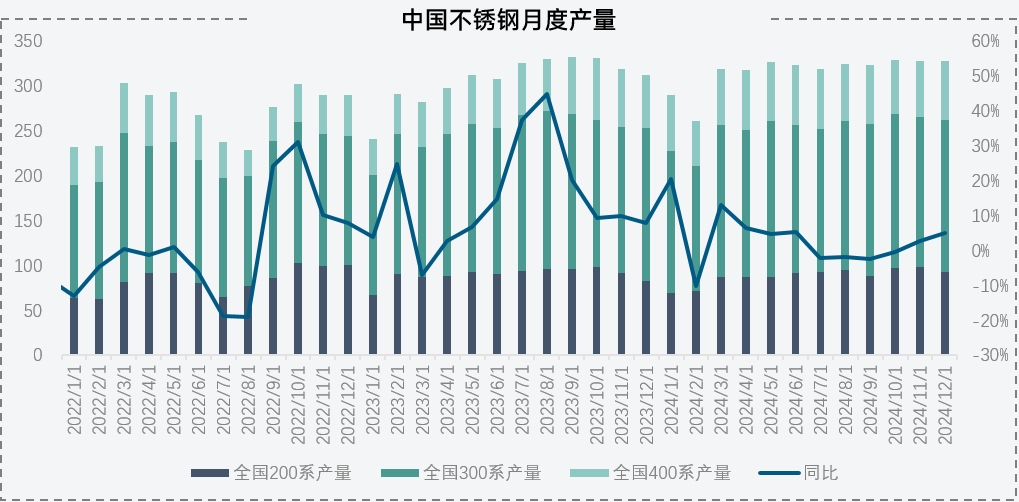

In 2023, stainless steel production increased significantly by 4.35 million mt YoY, a growth of over 13%. Although this year's growth will not match that of 2023, production remains at a high level, with 2024 stainless steel production expected to approach 38 million mt, up 1.05 million mt YoY, an increase of 3%. Chromium demand in metal content reached 6.5 million mt (equivalent to approximately 13 million mt of high-carbon ferrochrome in physical terms). Currently, demand for ferrochrome remains high amid the growth in stainless steel production.

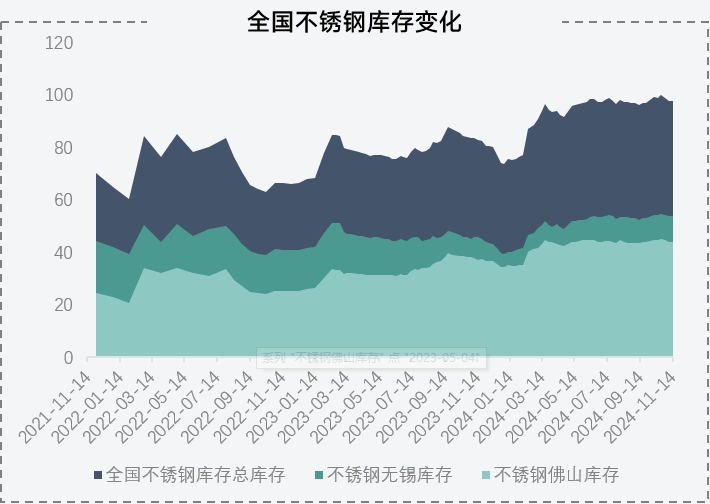

Stainless steel production remains at high levels, with social inventories gradually accumulating throughout the year. In November, social inventories in Wuxi and Foshan approached 1 million mt, up 140,000 mt YoY, an increase of 18%. Although stainless steel inventories have reached high levels and shown significant growth, they remain limited compared to the production increase this year. Despite ongoing market skepticism, particularly against the backdrop of a shrinking real estate sector, the growth in stainless steel production appears to align with downstream consumption. Based on current inventory levels and the stability of stainless steel production plans, market demand for stainless steel is expected to match current production levels.

Analysis of China's High-Carbon Ferrochrome Costs

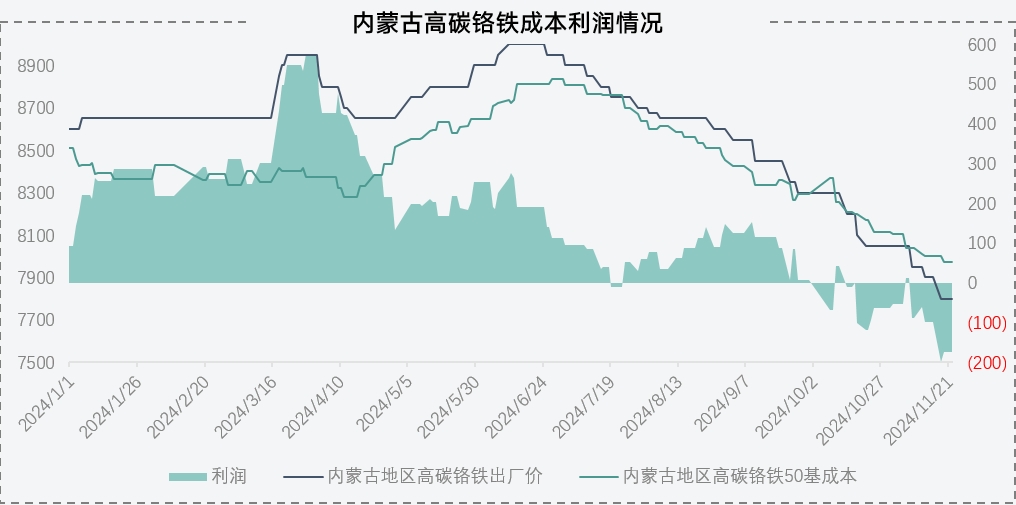

In H1 this year, supported by steel bidding prices, ferrochrome production profits performed well. For example, in Inner Mongolia, ferrochrome enterprises enjoyed sustained profitability, with production profits reaching 547 yuan/mt (50% metal content) by the end of March. Driven by substantial profits, many ferrochrome manufacturers actively expanded production, making H1 a peak period for new production line launches. However, the allure of profits led to severe supply surpluses in the ferrochrome market, causing prices to decline continuously, with recent losses of approximately 173 yuan/mt (50% metal content).

Currently, most facilities in Inner Mongolia are large submerged arc furnaces with high production stability. Enterprises have signed agreements with power suppliers requiring them to meet at least 70% of their electricity usage targets, or face penalties. Additionally, the costs of shutting down and restarting large furnaces are high, especially in winter when cooling water may freeze. As a result, production typically continues through year-end. Enterprises also hold long-term contracts for chrome ore, necessitating production to generate cash flow, making continuous production crucial. Despite market losses, production adjustments in Inner Mongolia remain limited, with most enterprises persisting in operations.

Analysis of China's Chrome Ore Supply

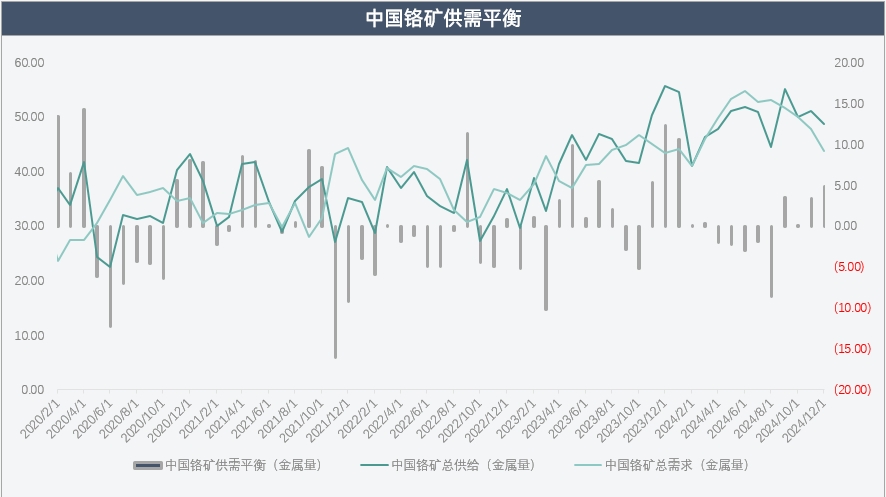

From January to November 2024, cumulative chrome ore imports reached 18.9403 million mt, up 2.6 million mt YoY, an increase of 15.94%. Annual imports are expected to exceed 20 million mt. Notably, chrome ore imports in 2023 increased by 3.33 million mt compared to 2022, a growth rate of 22%, marking two consecutive years of significant growth. Driven by high profits and strong domestic demand, chrome ore imports are expected to remain at high levels.

Despite rising chrome ore imports, the buffering effect of port inventories has nearly disappeared, with port chrome ore inventories consistently below 3 million mt in recent years. A significant portion of these inventories serves as raw material stock for ferrochrome plants, leaving limited quantities available for trading. Additionally, with rising domestic ferrochrome production, demand for chrome ore has increased, causing the inventory-to-sales ratio to drop to approximately 1.2 during the year. This has made the relationship between inventory and prices more directly correlated.

Chrome Ore Supply-Demand Balance

Since 2022, the chrome ore market has been characterized by robust supply and demand. In 2024, the fine ore market is expected to maintain a tight supply-demand balance, with a potential supply gap of only 24,600 mt in metal content.

Although chrome ore production remains profitable, supply is highly concentrated, with foreign suppliers maintaining strong control over the market. Additionally, the increasing trend of chrome ore transshipment through Singapore in recent years has allowed greater flexibility in controlling supply to China.

Currently, the chrome ore market exhibits low inventories and a tight supply-demand balance in the short term. However, considering the supply-demand balance for stainless steel, domestic chrome ore is already in significant surplus. This surplus has been absorbed by the substantial increase in ferrochrome production this year, but ferrochrome has not been effectively consumed. The current price inversion in ferrochrome has led to production cuts, reducing demand for chrome ore. This pressure is expected to gradually spread upstream to the chrome ore market, revealing supply-demand imbalances.

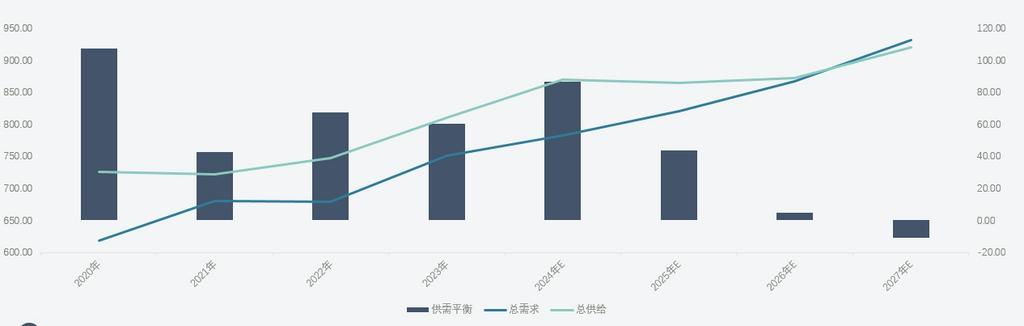

China's High-Carbon Ferrochrome Supply-Demand Balance

In 2024, high-carbon ferrochrome faced severe supply surpluses, with cumulative surpluses expected to exceed 700,000 mt in metal content, equivalent to approximately 1.4 million mt of high-carbon ferrochrome (50% metal content).

From April to July, high bidding prices for steel led to significant increases in both domestic and imported high-carbon ferrochrome, resulting in a notable surplus for the year.

Currently, the surplus is primarily concentrated in downstream stainless steel mills, further strengthening their pricing power over ferrochrome. With low stainless steel mill profits and a strong desire to bargain down raw material prices, ferrochrome manufacturers are struggling to maintain profitability.

Based on current surplus levels and the low willingness of Inner Mongolia's ferrochrome manufacturers to cut production, the process of restoring supply-demand balance is expected to be relatively slow. Market supply is likely to remain loose until at least Q1 2025.

Global High-Carbon Ferrochrome Supply-Demand Balance

Globally, the high-carbon ferrochrome market is expected to continue experiencing robust supply and demand in the coming years. On the supply side, Chinese ferrochrome enterprises are actively expanding overseas, establishing new plants in Zimbabwe and Indonesia. Domestically, numerous approved but yet-to-be-constructed ferrochrome production lines will also drive supply growth. On the demand side, the stainless steel industries in China and Indonesia remain in expansion, with ongoing substitution of low-end steel grades by stainless steel. Particularly, the increasing share of 300-series stainless steel will further boost demand for ferrochrome.

As global ferrochrome production rises, demand for chrome ore raw materials is also increasing. However, due to the concentration of chrome ore resources and limitations in mining exploration, extraction, overseas transportation, and beneficiation infrastructure, the imbalance between chrome ore supply and demand is expected to persist in the short term, keeping chrome ore prices relatively high. In recent years, the rapid expansion of new ferrochrome capacity, coupled with the lack of decommissioning of old capacity, has led to significant overcapacity. This is expected to impact the profitability of global ferrochrome smelters, with notable cost differences emerging between regions and plants.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)